Balancing Ambition and Reality: A Financial Deep Dive into the Lives of Brian and Michael

For many, the path to adulthood is paved with a complex mix of career aspirations, personal milestones, and the persistent, often daunting reality of financial management. Brian and Michael, a 34-year-old couple living in central Connecticut, find themselves at such a crossroads. Having been together since 2013, the couple is preparing to celebrate their 10-year anniversary this November. While they have successfully navigated the complexities of life in the public and non-profit sectors, they currently find themselves grappling with the weight of consumer debt and the elusive dream of home ownership.

This case study examines their current financial landscape—a narrative of professional growth, personal resilience, and the search for a sustainable path toward long-term security.

The Human Context: Who Are Brian and Michael?

Brian and Michael are two individuals deeply committed to their work and their community. Michael, a project coordinator for a state behavioral health agency, is also an active advocate and disability leadership coordinator. As a brain injury survivor who has personally navigated mental health challenges, his professional life is driven by a passion for supporting young people. Brian, equally dedicated, serves as a quality assurance manager for a state-run hospital.

Their lives are filled with intellectual and creative pursuits. Michael is an avid reader and collector who enjoys cooking, drawing, and gaming. Brian, a native of the Boston area and a product of a large Irish Catholic family, is a lifelong learner who finds joy in hiking, gardening, and community engagement. Despite their achievements, both men feel a palpable sense of "stuckness." They are eager to unlock the next level of adult life—which they define as achieving permanent debt freedom and securing a home of their own.

Chronology of Challenges: A Year of Transition

The last twelve months have been a period of significant upheaval for the couple. In 2022, they were living in a comfortable, 600-square-foot studio apartment for $945 per month. Their long-term financial roadmap included plans to enter the housing market in late 2023. However, life intervened.

The couple spent three-and-a-half months navigating the volatile 2022-2023 rental market, eventually moving into a spacious, two-bedroom, two-bathroom apartment in a converted historic mill. While the new space offers industrial charm, 12-foot ceilings, and a dedicated home office, the transition was costly. Coupled with unexpected veterinary expenses for their two kittens, these events significantly impacted their liquid savings and forced them to re-evaluate their timeline for home ownership.

Supporting Data: An Analytical Look at the Numbers

A clear picture of their financial health requires a granular look at their income and liabilities. The couple boasts a robust combined gross annual income of $167,544, with a net annual income of approximately $109,455.

Debt Profile

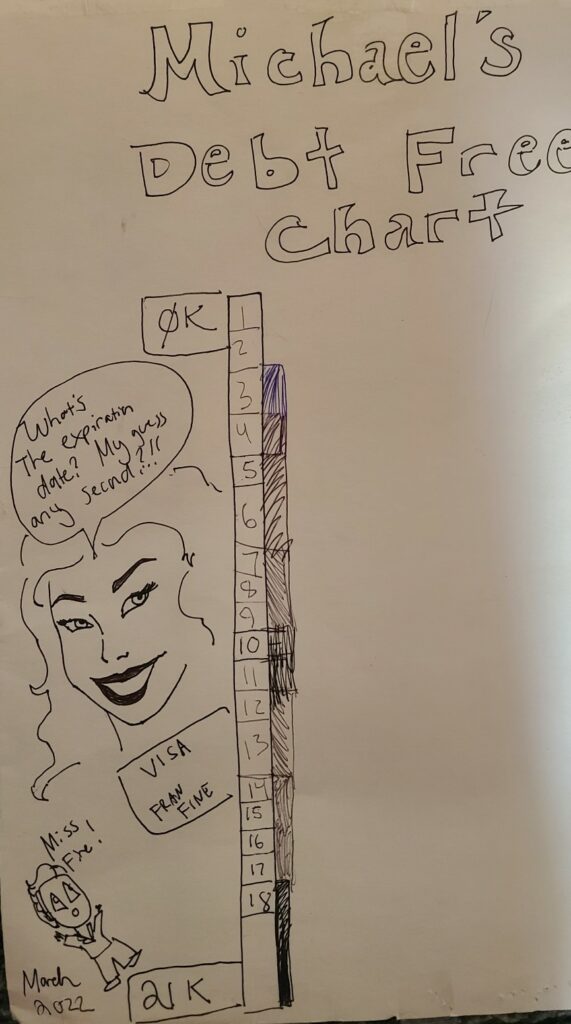

The primary source of stress is their consumer debt, which currently totals $28,259. This includes:

- Brian’s Visa (SCU): $16,057 balance (currently 0% APR, but rising to 17.99% in November).

- Michael’s Visa Platinum: $9,700 balance (10.99% interest).

- Brian’s Visa Platinum (Navy Federal): $2,503 balance (0.99% interest, rising to 17.74% in November).

Asset Allocation

Despite their debt, the couple has managed to build a respectable base of assets totaling $91,250, primarily through retirement vehicles. These include a combination of 401(k) accounts, a pension, a 457, a 403b, and various health savings accounts (HSAs). Their current monthly expenditure stands at $8,035, leaving them with an annual surplus—if managed correctly—of roughly $13,000.

Expert Analysis: A Framework for Financial Stability

The request for a "Financial Tune-up" brings us to the core of the dilemma. Liz, a seasoned voice in the personal finance space, suggests that while Brian and Michael feel a sense of shame regarding their financial position, their situation is far from catastrophic.

The Power of Expense Tracking

The first and most critical recommendation is the implementation of a rigorous expense tracking system. By using tools like Empower (formerly Personal Capital) or simple spreadsheet methods, the couple must identify where every dollar is going. The goal is to move away from "frittering away" money on discretionary items and toward intentional spending that aligns with their life goals.

The Debt Payoff Strategy

Liz proposes a "no-spend" or austerity approach for the short term. By categorizing expenses into Fixed, Reducible, and Discretionary, she identifies an opportunity to reduce their monthly spending from $8,035 to $6,665. This adjustment, combined with their current debt repayment allocations, would allow the couple to direct $4,456 per month toward their creditors. At this rate, the couple could be entirely debt-free in approximately six-and-a-half months.

Implications: The Path Toward Future Goals

The implications of this strategy extend far beyond simple debt repayment. By clearing their balance sheets, Brian and Michael would create the necessary "buffer" to build an emergency fund, which is the cornerstone of any long-term home-buying plan.

Addressing the "Master’s Degree" Question

A significant point of contention for Brian is the pursuit of a graduate degree. The expert consensus is clear: unless there is a guaranteed, documented, and significant salary increase directly linked to the degree, it should be avoided. For someone with the goal of becoming debt-free and owning property, the time and financial cost of a master’s degree represent an "unhelpful detour."

Retirement and Long-Term Security

Brian and Michael have access to the "triple crown" of retirement vehicles: a 403b, a 457, and a pension. These are powerful tools. However, they must be managed with an eye toward low-expense ratios and strategic asset allocation. Furthermore, Brian should prioritize rolling his old 401(k) into an IRA to gain greater control over his investment choices.

The Philosophy of "Enough"

Ultimately, the advice provided highlights a crucial truth: money is a component of a well-lived life, not the solution to it. The couple’s stress stems not from a lack of potential, but from a cycle of "feast and famine." By identifying their long-term priorities—marriage, a home with a garden, and a lasting legacy—and learning to spend in accordance with those goals, they can escape the cycle of financial shame.

Conclusion: A Future Built on Intentionality

Brian and Michael are at an inflection point. Their combined income is strong, their benefits are enviable, and their long-term goals are clear. By embracing a period of disciplined spending and prioritizing their debt, they can transform their current anxiety into a robust plan for the future. The transition from a studio apartment to their current home signifies their growth; the next step is to ensure that their financial habits grow to match their aspirations. With the right systems in place, the dream of owning a home and achieving lasting financial independence is not just possible—it is well within their reach.