Thematic Investing 2.0: From Niche Speculation to Core Portfolio Architecture

For over a decade, thematic investing was viewed by many institutional and retail investors alike as a "sidecar" strategy—a way to add a bit of spice to a traditional, diversified portfolio. The narrative was dominated by broad, catch-all categories like "disruptive technology" or early-stage artificial intelligence. However, as the global economy undergoes a rapid, technology-driven structural transformation, the approach to thematic investing is maturing. We are entering the era of Thematic Investing 2.0, where precise, targeted exposure to fundamental building blocks—memory, robotics, and the orbital economy—is replacing generic tech exposure.

Recent insights from the TMX VettaFi Midyear Symposium underscore this shift. The conversation among financial advisors has moved beyond the existential "should we allocate?" toward the more practical "how much should we allocate?" This transition signals that thematic strategies are no longer considered speculative bets, but rather sophisticated, surgical instruments for long-term growth.

The Data: A Shift in Portfolio Construction

The findings from the TMX VettaFi Midyear Symposium offer a compelling look at current advisor sentiment. A poll conducted during the event revealed that nearly three-quarters (73%) of respondents now maintain a dedicated allocation to thematic strategies within their clients’ average portfolios.

While the majority of this capital (44.8%) is still housed within the "core-satellite" framework—typically representing a 1% to 5% allocation—there is a growing cohort of advisors who are going deeper. Nearly 30% of surveyed advisors have increased their thematic footprint to 6% or more of the overall asset mix. This reflects a growing confidence in the durability of these specific, non-cyclical trends.

Breakdown of Advisor Thematic Exposure

| Average Client Portfolio Exposure | % of Responses |

|---|---|

| 0% (No exposure) | 26.9% |

| 1% – 5% (Core satellite/tactical) | 44.8% |

| 6% – 10% (Meaningful structural tilt) | 19.4% |

| More than 10% (High-conviction allocation) | 9% |

The data indicates a clear hierarchy of conviction. The 9% of advisors committing more than 10% of portfolios to these themes suggest a belief that these sectors are not merely "trends," but foundational shifts in how global productivity will be measured in the coming decades.

Chronology of a Market Pivot: Moving Beyond Generalization

The evolution of thematic investing follows a logical chronology. In the mid-2010s, thematic funds were often broad, high-beta products that moved in lockstep with the NASDAQ. When the market dipped, these "innovation" funds suffered disproportionately.

However, the post-pandemic economic environment—characterized by labor shortages, geopolitical nearshoring, and the massive data-processing requirements of generative AI—forced a reckoning. Investors realized that a broad tech ETF was no longer enough. To capture the true value of the next industrial revolution, one needed to own the enablers of the technology, not just the front-end software providers. This realization led to the current focus on the hardware stack, the automation of the supply chain, and the expansion of the space-based connectivity layer.

The Pillars of Modern Thematic Exposure

DRAM: The Hardware Bottleneck

It is a common misconception that the AI revolution is entirely software-driven. In reality, the software is only as fast as the physical hardware allowed to process and store data. This is where Dynamic Random Access Memory (DRAM) becomes critical.

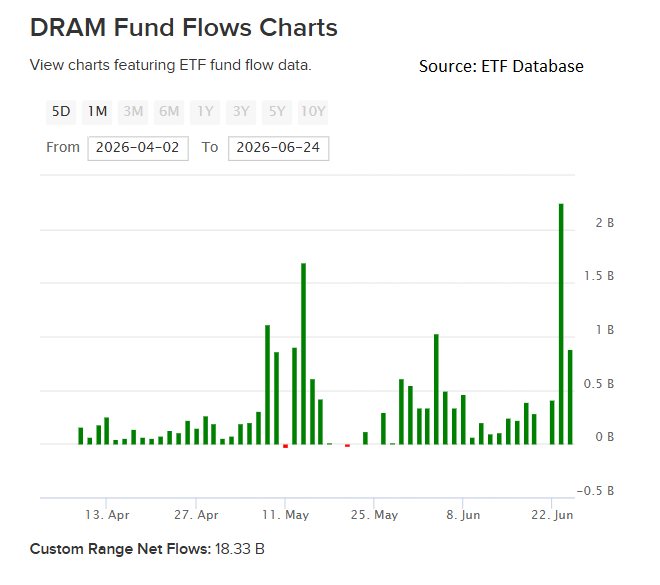

The Roundhill Memory ETF (DRAM) has emerged as a focal point for investors looking to participate in the AI boom without taking on the volatility of pure-play software companies. Since its inception less than three months ago, the fund has attracted over $18 billion in net flows. The logic is straightforward: as the demand for AI infrastructure accelerates, high-performance memory is increasingly viewed as the most significant technological bottleneck. By targeting global memory and storage manufacturers, DRAM provides a precise vector into the "pick-and-shovel" segment of the AI supply chain.

ROBO: The Automated Reality

The second pillar is the total integration of robotics. Zeno Mercer, senior research analyst at VettaFi, has frequently highlighted that robotics has moved from a "futuristic concept" to a "mainstream necessity."

The ROBO Global Robotics and Automation Index ETF (ROBO) captures this evolution. The fund, which manages approximately $2 billion in assets, moves beyond industrial arms. It covers the entire automation ecosystem, including computational sensing, machine vision, and logistics.

Why has this become a staple? The answer lies in macro-economic necessity. With aging demographics in developed nations and the global movement toward nearshoring—bringing manufacturing closer to home—companies are being forced to automate to survive. Robotics is no longer a luxury for efficiency; it is the only way to mitigate the structural labor shortages defining the 2020s.

UFO: The Orbital Frontier

The third pillar is arguably the most ambitious: the space economy. The Procure Space ETF (UFO) has gained traction by challenging the notion that space is the sole domain of governments.

Space exploration has transitioned into the commercialization of space. Today, the orbital economy is a foundational component of global defense, climate monitoring, and global connectivity networks. While investors are often drawn to the headlines surrounding companies like SpaceX, the value of the UFO ETF lies in its diversification across satellite operators, communication infrastructure, and aerospace hardware manufacturers like Trimble and Sirius XM. As commercial interests in low-Earth orbit (LEO) multiply, the thematic case for space-based connectivity is becoming a long-term secular trend that few diversified portfolios can afford to ignore.

Official Perspectives and Market Implications

The consensus among market analysts at VettaFi and other industry observers is that the integration of these themes is a response to the "efficiency imperative." In an era of high interest rates and wage inflation, companies that invest in robotics and advanced memory systems are fundamentally more efficient than their peers.

From an advisory standpoint, the implication is clear: the "60/40" portfolio of the 20th century is struggling to provide the growth necessary to keep pace with modern inflationary pressures. By carving out a "thematic sleeve," advisors are providing clients with exposure to long-term secular growth drivers that are largely uncorrelated with traditional equity market cycles.

However, this transition requires discipline. The shift from "should I allocate?" to "how much?" implies that advisors must now conduct rigorous due diligence on the purity of the thematic exposure. Not all thematic funds are created equal; the most successful ones, like those identified above, focus on specific, quantifiable supply chain segments rather than broad, thematic labels.

Conclusion: The New Standard for Long-Term Growth

The move toward memory, robotics, and space exploration represents a departure from speculative growth and a movement toward tangible, technology-enabled productivity. As the symposium data suggests, the thematic sleeve is becoming a standard feature of the modern client portfolio.

As we look toward the remainder of the decade, the winners in this space will be those who recognize that technological evolution is not a temporary disruption, but a permanent, compounding reality. For the individual investor and the professional advisor alike, the tools to capture this growth—through specialized instruments like DRAM, ROBO, and UFO—are more accessible than ever. Thematic investing has come of age, transitioning from a speculative experiment to a core, structural element of successful wealth management.

Disclaimer: VettaFi LLC ("VettaFi") is the index provider for the Procure Space ETF (UFO) and the ROBO Global Robotics and Automation Index ETF (ROBO), for which it receives an index licensing fee. However, UFO and ROBO are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of these ETFs. For deeper analysis on structural trends and portfolio building blocks, visit the VettaFi Thematic Content Hub.