The Biotech Renaissance: How AI and M&A Are Igniting a Sector-Wide Recovery

The biotechnology sector, having endured a grueling multiyear "winter" characterized by high interest rates, funding droughts, and regulatory skepticism, has officially staged a dramatic breakout. As macroeconomic headwinds subside and the path to profitability becomes clearer for clinical-stage firms, investors are flocking back to the space. Biotechnology exchange-traded funds (ETFs) are currently leading the market, driven by a powerful dual engine: the transformative efficiency of artificial intelligence in drug discovery and a relentless wave of corporate consolidation.

Main Facts: A Sector Transformed

The current surge in biotech is not merely a reflexive market bounce; it is a structural evolution. For years, the sector was hampered by the high cost of capital, which disproportionately punished small-cap firms burning through cash to fund clinical trials. Today, the landscape is fundamentally different.

The integration of generative AI and computational biology has fundamentally altered the economics of early-stage research. By predicting protein structures and modeling complex biological interactions with unprecedented speed, AI is slashing the "discovery" phase of drug development. This reduction in cost and timeline is essentially de-risking the portfolios of mid-sized and smaller firms, making them more attractive targets for Big Pharma.

Simultaneously, the regulatory environment has stabilized. With clarity on drug pricing policies and the anticipation of a more accommodative interest rate environment, large pharmaceutical corporations—sitting on significant cash reserves—have returned to the M&A arena with renewed vigor. This capital infusion is the primary catalyst for the current bull run in biotech indices.

Chronology: The Road to the Breakout

To understand the current momentum, one must look at the timeline of the sector’s recent history:

- 2021–2022 (The Great Correction): Following the pandemic-era euphoria, the biotech sector entered a sharp decline. Rising interest rates made the "growth-at-all-costs" model unsustainable, leading to massive valuation write-downs.

- 2023 (The Stabilization Phase): As inflation cooled, biotech firms shifted their focus toward fiscal discipline. Companies began streamlining pipelines and prioritizing "platform" technologies over speculative projects.

- Early 2024 (The AI Catalyst): AI-driven drug discovery platforms transitioned from experimental to essential. Major partnerships between tech-forward biotech firms and legacy pharma giants began to dominate the headlines.

- Mid-2024 (The M&A Surge): With the cost of capital declining, the "M&A wave" gained speed. Deals such as Novartis’s acquisition of Avidity Biosciences and Merck’s strategic move to purchase Terns Pharmaceuticals signaled to the market that the "buy vs. build" calculation had shifted decisively toward acquisition.

- June 2025 – Present: Biotech ETFs, particularly those focusing on clinical-stage breakthroughs, have posted historic one-year returns, outperforming broader market indices and signaling a long-term shift in sector sentiment.

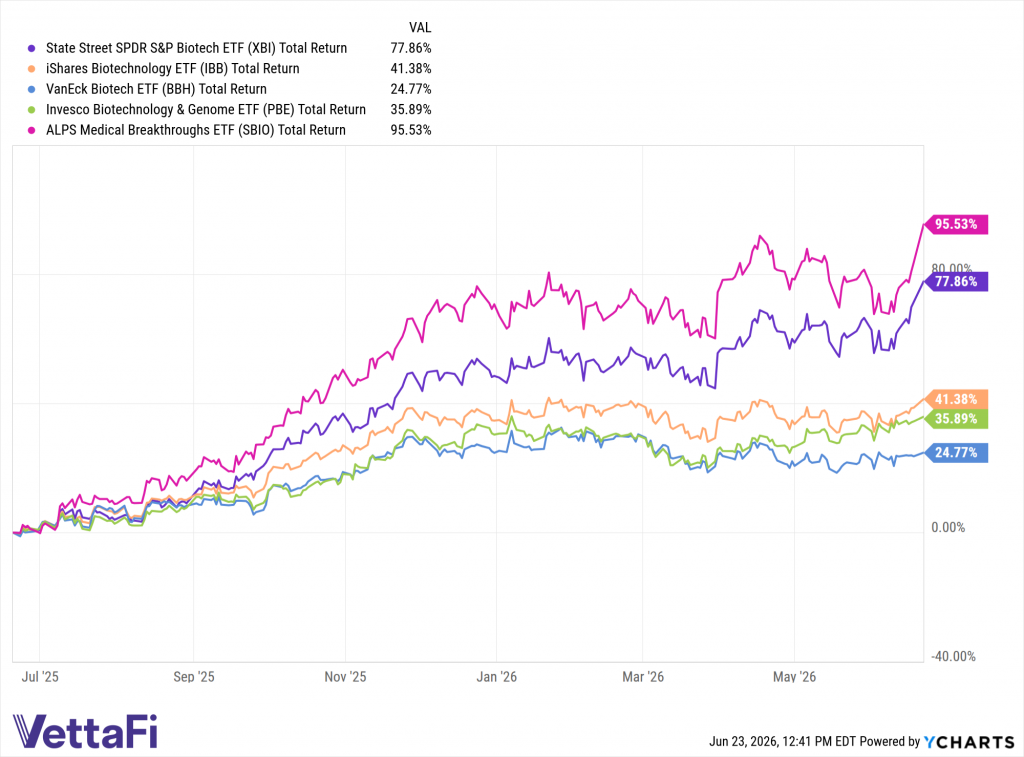

Supporting Data: Comparative ETF Performance

Selecting the right vehicle for biotech exposure is not a "one-size-fits-all" endeavor. Because index methodologies vary wildly, an investor’s return can depend heavily on whether their chosen fund targets "mega-cap" stability or "small-cap" innovation.

The Landscape of Major Biotech ETFs

As of the latest reporting period ending June 22, the performance divergence among major ETFs is stark:

- ALPS Medical Breakthroughs ETF (SBIO): The clear standout with a 95.5% return over the past year. SBIO’s strategy is unique; it explicitly targets companies in clinical phase II or III trials. By focusing on firms with active, high-potential pipelines, it captures the "acquisition premium" when these firms are bought out by larger entities.

- State Street SPDR S&P Biotech ETF (XBI): As the largest fund in the segment with $9 billion in AUM, XBI utilizes an equal-weight strategy. This offers broad, democratic exposure across large, mid, and small-cap stocks, avoiding the concentration risk associated with market-cap weighting. It returned 77.9% over the past year.

- iShares Biotechnology ETF (IBB): With $8.1 billion in assets, IBB favors established mega-cap firms. While it provides the stability of industry giants, it returned a more moderate 41.4%.

- Invesco Biotechnology & Genome ETF (PBE): Utilizing a multi-factor approach, PBE focuses on firms engaged in R&D and genetic engineering. It yielded a 35.9% return.

- VanEck Biotech ETF (BBH): Concentrated in commercialized giants like Amgen and Gilead Sciences, BBH serves as a proxy for established commercial success rather than speculative pipeline growth, returning 24.8%.

Official Perspectives and Industry Strategy

Industry experts suggest that the current consolidation is not a temporary trend but a necessary structural shift. "The days of ‘spray and pray’ venture capital in biotech are over," says one industry analyst. "Today, Big Pharma needs to restock their pipelines to replace drugs facing patent cliffs. They aren’t looking to reinvent the wheel; they are looking to acquire companies that have successfully leveraged AI to de-risk the early stages of clinical development."

From an index provider perspective, the success of funds like SBIO highlights that investors are increasingly sophisticated. They are no longer looking for "beta" exposure to the whole sector; they are looking for "alpha" exposure to companies that have reached the clinical validation stage. By filtering for Phase II and III trials, these ETFs essentially serve as a curated list for potential M&A targets.

Implications for the Future

The implications of this shift are profound for both the retail investor and the broader healthcare ecosystem:

1. The Rise of the "Computational Biotech"

The next decade will likely be defined by the "Tech-Bio" convergence. Firms that successfully bridge the gap between silicon-based AI modeling and bench-side biological validation will command the highest valuations. Investors should look beyond traditional pharmaceutical metrics (like revenue and P/E ratios) and begin evaluating companies based on their proprietary AI datasets and intellectual property in protein folding and gene editing.

2. Continued M&A Intensity

The M&A wave is expected to continue as long as interest rates remain stable or trend lower. Large pharmaceutical companies face a "patent cliff" in the coming years, meaning they must acquire external innovation to maintain growth. Small and mid-cap biotech firms that successfully navigate clinical hurdles will remain in the crosshairs of these corporate giants.

3. Increased Volatility and Dispersion

While the sector is currently in a bull phase, investors must be wary of the inherent risks of biotech. Clinical trial failures remain the most significant threat to individual stock valuations. The dispersion between the winners (those bought out or achieving FDA approval) and the losers (those with failed trials) will widen. Consequently, the choice of an ETF—specifically one that employs a robust, methodology-driven approach—is more critical than ever.

4. Regulatory Vigilance

While the regulatory environment has stabilized, the long-term impact of new drug pricing legislation remains a variable. Investors should monitor how these policies affect the profit margins of commercialized firms (like those found in IBB and BBH) versus the R&D incentives for smaller innovators (like those in SBIO).

Conclusion: A New Chapter for Life Sciences

The biotechnology sector has successfully transitioned from a period of defensive posturing to one of offensive growth. The combination of AI-enabled R&D, a resurgence in M&A activity, and a stabilizing macroeconomic environment has created a fertile ground for investors.

However, the "biotech breakout" is not a uniform wave. As demonstrated by the significant performance gap between funds like SBIO and BBH, the methodology behind an ETF is the defining factor of success. Investors who prioritize firms with tangible, clinical-stage progress—and who understand the structural shift toward computational drug discovery—are best positioned to navigate the next phase of this sector’s evolution.

As the industry continues to integrate deep learning into the heart of the R&D process, the line between technology and medicine will continue to blur, likely leading to more rapid breakthroughs and, consequently, more frequent and lucrative opportunities for consolidation. For those willing to navigate the inherent volatility, the biotech sector offers a compelling, high-growth frontier in the modern investment landscape.

Disclaimer: VettaFi LLC is the index provider for SBIO, for which it receives an index licensing fee. This article is for informational purposes only and does not constitute financial advice. Investors should conduct their own due diligence or consult with a financial advisor before making investment decisions.