The Anti-Debt Investor: How Lucy Hinds Retired in Three Years by Flipping the Script

In the world of real estate investing, the "Dave Ramsey" school of thought—prioritizing zero debt and total liquidity—is often viewed as the antithesis of aggressive wealth building. Yet, for Cincinnati-based investor Lucy Hinds, this conservative upbringing provided the foundational discipline necessary to pull off an extraordinary feat: retiring from her W2 career in just over three years by strategically leveraging the very debt she was once taught to avoid.

Hinds’ journey is a masterclass in calculated risk, the power of the Home Equity Line of Credit (HELOC), and the importance of knowing when to stop chasing growth in favor of lifestyle design.

The Catalyst: A Shift in Financial Philosophy

For years, Hinds lived by a rigid financial playbook: aggressive saving, no consumer debt, and a deep-seated fear of leverage. However, after reading Robert Kiyosaki’s seminal work, Rich Dad Poor Dad, her perspective on capital allocation underwent a seismic shift. She realized that while she had been saving diligently, she was leaving her primary asset—her home—underutilized in an era of post-pandemic appreciation.

With significant equity locked in her Cincinnati residence, Hinds made a pivot that defied her previous financial conditioning. She secured a $176,000 HELOC, effectively converting her "dead" equity into "active" capital. This decision was not made out of recklessness, but rather a calculated assessment of market potential. In a blistering 90-day period between July and September 2022, she deployed that capital to acquire three single-family rental properties.

Remarkably, by the time her first mortgage payment was due, all three properties were already generating cash flow, setting a blistering pace for her financial independence.

Chronology of an Accelerated Portfolio

The speed of Hinds’ entry into the market was as noteworthy as her selection criteria. Her approach prioritized immediate cash flow over long-term speculative appreciation, ensuring that her debt service was covered from day one.

The Initial Sprint (July – September 2022)

Hinds’ first three acquisitions set the tone for her portfolio’s performance:

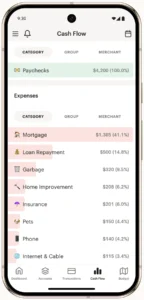

- Property One: A three-bed, two-bath home acquired for $215,000. Hinds utilized a 25% down payment ($54,000) sourced from her HELOC and cash savings. With a monthly mortgage of $1,227 and a rental income of $2,150, the property generated $923 in monthly cash flow.

- Property Two: A fully turnkey home purchased for $240,000. Because the asset required zero capital expenditure for repairs, it became an immediate revenue generator. With a mortgage of $1,480 and rent of $2,225, it added $750 to her monthly bottom line.

- Property Three: A townhome acquisition costing $157,000. While this required a $10,000 renovation budget, the yield remained strong. With a mortgage (including HOA fees) of $1,288 and rent at $2,050, it contributed $762 to the monthly cash flow.

The Strategic Pause (2023 – 2025)

Following the initial sprint, Hinds deliberately slowed her acquisition pace. The mounting balance of her HELOC and the exhaustion of managing three rapid-fire renovations while maintaining a full-time job served as a reality check.

"I wanted to let the dust settle," Hinds explains. She spent the better part of a year focusing on debt reduction, using the portfolio’s cash flow to pay down the HELOC. She did not acquire her fourth property until July 2023. By this time, interest rates had surged to 7.5%, but Hinds remained unfazed. She acquired a $235,000 turnkey property that still yielded $550 in monthly cash flow, proving that in her model, sound property fundamentals consistently trumped macroeconomic rate fluctuations.

Data-Driven Discipline: The "Reinvestment" Secret

What separates Hinds from many novice investors is her refusal to "lifestyle creep" during the early stages of growth. While many investors begin withdrawing cash flow to upgrade their personal vehicles or vacations as soon as they see their first monthly surplus, Hinds practiced extreme fiscal restraint.

Every dollar generated by her portfolio was funneled back into the business. This reinvestment strategy accomplished two critical goals:

- HELOC De-leveraging: By systematically paying down the line of credit, she reduced her interest-rate risk.

- Capital Reserves: By avoiding personal withdrawals, she built a war chest that allowed her to absorb maintenance costs or vacancy periods without dipping into her personal savings.

This discipline was the engine of her early retirement. By keeping her personal standard of living static while her portfolio’s income grew exponentially, she achieved the "crossover point"—where passive income equals total expenses—in just 38 months.

Implications: Defining "Enough" in Real Estate

Perhaps the most unconventional aspect of Hinds’ story is her decision to cap her portfolio at five properties. Most investors are conditioned to believe that "more is better" and that they should scale until they reach a specific arbitrary goal, such as 10 or 20 units.

Hinds conducted a rigorous ROI assessment and realized she had already reached her destination. "Knowing you’re enough is the whole game," she reflects. Instead of acquiring more, she opted to sell one property to pay off the mortgage on her primary residence. This strategic move eliminated her largest personal monthly liability, effectively lowering her "burn rate" and increasing her financial resilience.

Current Portfolio Impact

- Total Annual Income: $45,352.

- Personal Spending: $40,000 (chosen lifestyle).

- The Surplus: Hinds now reinvests the remaining $5,352 annually toward future goals, including the purchase of a Florida vacation home, which she intends to convert into a primary residence in the coming years.

Official Responses and Industry Outlook

When asked about the sustainability of her model, Hinds emphasizes the importance of self-management. By acting as her own property manager—handling tenant relations, lease signings, and maintenance coordination—she keeps overhead low. While she occasionally employs a handyman or plumber for specialized tasks, the bulk of the management burden remains with her, allowing her to maintain a direct pulse on the health of her assets.

For aspiring investors, Hinds’ path provides a blueprint for what is possible when you combine the traditional, conservative mindset of the "debt-averse" with the aggressive tools of the "real estate professional."

The Path Forward

Hinds’ husband continues to work, with a retirement date set for early 2029. In the interim, the couple is not chasing the next "big deal." Instead, they are focused on optimizing the current portfolio, ensuring that their five doors remain high-performing assets that fund their desired lifestyle.

Her story serves as a vital reminder to the investment community: Real estate is not merely a vehicle for building the largest possible empire—it is a tool for building the life you want. By defining her terms early and refusing to be lured into the "growth for growth’s sake" trap, Lucy Hinds has successfully retired on her own terms, proving that sometimes, the smartest move is knowing when you have finally arrived.

Conclusion

The transition from a debt-averse, "Dave Ramsey" style saver to a successful real estate investor is not a common narrative, but it is one that proves highly effective when executed with Hinds’ level of precision. By leveraging equity to secure assets, refusing to touch cash flow until the portfolio was self-sustaining, and recognizing when "enough is enough," Hinds has unlocked a level of freedom that many investors with 50-door portfolios are still chasing. Her journey is a testament to the fact that financial independence is not measured by the number of properties on a spreadsheet, but by the security and freedom of the life those properties provide.