Automated Wealth Management via Spreadsheets: An In-Depth Analysis of Tiller Money’s Financial Ecosystem

In an era dominated by proprietary, closed-loop financial applications, a growing segment of consumers is returning to the foundational tool of modern computing: the spreadsheet. While modern fintech apps offer slick interfaces, they often restrict user control, limit customization, and monetize user data.

Tiller Money addresses this gap by bridging the gap between automated bank feeds and user-controlled spreadsheets. This analysis evaluates Tiller Money’s architecture, operational mechanics, historical context, security protocols, and broader implications for the personal finance industry.

Main Facts: What is Tiller Money?

Tiller Money is a financial technology platform that automatically aggregates transaction and balance data from a user’s financial institutions and feeds it directly into Google Sheets or Microsoft Excel. Unlike traditional personal finance software, Tiller does not confine users to a rigid, pre-built dashboard. Instead, it acts as a secure data pipeline, giving users raw, organized financial data to manipulate as they see fit.

+-------------------------------------------------------------+

| Tiller Money Engine |

+-------------------------------------------------------------+

|

+---------------------+---------------------+

| |

v v

+------------------------+ +------------------------+

| Google Sheets Feeds | | Microsoft Excel Feeds |

+------------------------+ +------------------------+

| |

+---------------------+---------------------+

|

v

+-------------------------------------------------------------+

| Customizable Workbooks |

| - Foundation Template - AutoCat (Auto-categorization)|

| - Net Worth Dashboards - Custom Budgeting (50/30/20) |

+-------------------------------------------------------------+Core Value Proposition and Problem Resolution

For decades, personal finance enthusiasts tracking their money via spreadsheets faced three systemic bottlenecks:

- Manual Data Entry: The tedious and error-prone process of manually logging every credit card transaction, bank debit, and investment fluctuation.

- Template Design Overhead: The difficulty of building formulas, charts, and dashboards from scratch that remain functional over long periods.

- Analytical Constraints: The lack of dynamic tools to perform advanced financial modeling, such as debt snowball calculations or multi-year net worth tracking, without complex programming knowledge.

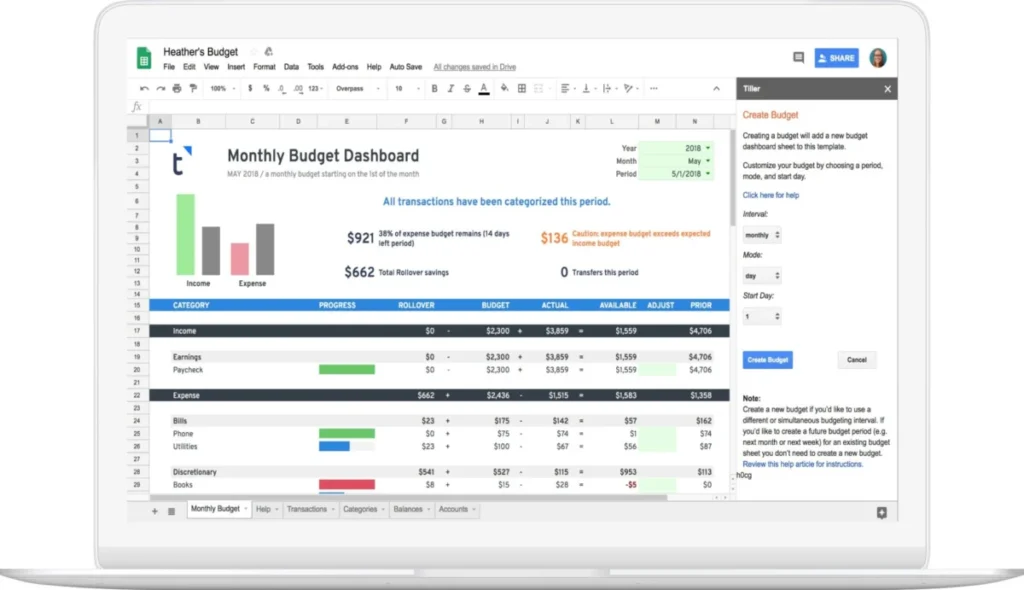

Tiller solves these pain points by establishing a secure read-only link to financial institutions, automating data delivery, and providing a highly extensible framework called the Tiller Foundation Template. This template provides users with pre-configured sheets for budgeting, net worth tracking, and transaction classification, while leaving the underlying workbook fully customizable.

Chronology: The Evolution of Spreadsheet-Based Budgeting

The development of Tiller Money and the broader shift toward automated spreadsheet budgeting has unfolded over several distinct phases:

Phase 1: The Era of Manual Data Manipulation (Pre-2010s)

Historically, personal finance tracking was divided into two camps: monolithic desktop software (such as Quicken and Microsoft Money) and custom-built Excel spreadsheets. While desktop software offered automation, it lacked flexibility and cross-platform compatibility. Conversely, spreadsheets offered infinite customization but required manual CSV downloads from bank websites and tedious data cleaning.

Phase 2: The Aggregation Revolution and the "Mint Era" (2010–2015)

The rise of web-based aggregators like Mint.com popularized automated financial tracking. However, these platforms operated within "walled gardens." Users could view their data but could not easily export, manipulate, or build custom models with it. Power users grew frustrated with rigid categorization algorithms and invasive advertising models.

Phase 3: The Birth of Tiller and the Rise of Open Feeds (2015–Present)

Recognizing the limitations of closed platforms, Tiller Money was founded to give users ownership of their data. When Tiller first debuted at major personal finance conferences like FinCon, many industry experts and bloggers were initially skeptical. The concept of linking live bank credentials to a Google Sheet felt unfamiliar and complex.

Over time, Tiller simplified its onboarding process, transitioning from a basic data-dump tool to a robust ecosystem. Key milestones in this evolution include:

- The Launch of the Foundation Template: Replacing fragmented starter sheets with a unified, robust framework for budgeting and tracking.

- The Introduction of AutoCat: A rules-based engine allowing users to automate transaction categorization using custom criteria.

- The Creation of Tiller Money Labs: A community-driven incubator that delivers advanced add-ons, such as debt planners, retirement projection models, and business expense trackers.

Supporting Data: Operational Mechanics, Security, and Pricing

To evaluate Tiller’s viability as a primary financial tool, it is necessary to examine its technical architecture, security protocols, and cost structure.

Technical Architecture and Account Integration

Tiller connects to financial institutions using Yodlee, a financial data aggregation platform utilized by nine of the fifteen largest banking institutions in the United States.

+--------------------+ Yodlee API +--------------------+

| User's Financial | ---------------------> | Tiller Money |

| Institutions | (Read-Only Access) | Engine |

+--------------------+ +--------------------+

|

| Secure Delivery

v

+--------------------+

| Google Sheets |

| or |

| MS Excel Workbook |

+--------------------+Through this integration, users can link:

- Checking and savings accounts

- Credit cards

- Investment portfolios and brokerage accounts

- Mortgages, student loans, and other liabilities

A key design feature of Tiller is the separation of account connection and spreadsheet integration. Connecting an account to the Tiller console does not automatically dump data into every workbook. Instead, users can link specific accounts to specific spreadsheets (up to five active workbooks per subscription). This architecture allows for clean separation of personal budgets, business entities, and long-term investment portfolios.

Feature Deep-Dive

| Feature | Description | Primary Use Case |

|---|---|---|

| Foundation Template | A pre-built workbook featuring Insights, Transactions, Categories, Monthly Budget, and Yearly Budget tabs. | Out-of-the-box setup for immediate budgeting. |

| AutoCat | An automated categorization engine based on user-defined keywords and description rules. | Eliminates manual sorting of recurring transactions (e.g., utility bills, subscriptions). |

| Tiller Money Labs | An experimental add-on repository offering community-built and official financial modules. | Advanced financial planning, including debt payoff and retirement modeling. |

| Multi-Book Architecture | The ability to feed distinct financial data streams into up to five separate spreadsheets. | Separating personal household finances from small business bookkeeping. |

Security Protocols

Because financial data aggregation requires access to sensitive information, Tiller employs bank-grade security measures:

- Data Encryption: All data transmitted between financial institutions, Tiller, and the user’s spreadsheet is protected using 256-bit AES encryption.

- Read-Only Restriction: Tiller’s access to connected accounts is strictly read-only. The platform cannot initiate transfers, pay bills, or modify account structures.

- Credential Protection: Tiller never stores or views bank login credentials; these are processed securely through Yodlee’s tokenized authentication framework.

- Two-Factor Authentication (2FA): Tiller supports multi-factor authentication, prompting users for temporary codes generated by SMS or authenticator apps during account refreshes.

Cost-Benefit Analysis

Tiller Money operates on a subscription-based pricing model:

- Trial Period: 30-day free trial with full functionality.

- Annual Subscription: $79 per year (equivalent to approximately $6.58 per month).

Unlike free personal finance platforms, Tiller does not display ads, cross-sell financial products, or sell user transaction data to third-party marketing firms. The subscription model aligns the company’s financial incentives with user privacy.

Official Responses and Corporate Philosophy

Tiller Money’s corporate philosophy centers on financial privacy, user autonomy, and the democratization of data.

Data Ownership and Privacy

In official documentation and public statements, Tiller emphasizes that the user, not the platform, owns the financial data. Tiller’s engineers do not access, analyze, or aggregate user spreadsheet data unless explicitly authorized by the user for technical support purposes.

This privacy-first approach is a response to the shifting landscape of fintech, where platforms frequently monetize user profiles to recommend credit cards, loans, and insurance policies.

The Role of Community-Driven Development

Tiller’s development team has adopted an open-source ethos regarding template creation. Rather than relying solely on in-house developers to build new features, the company actively fosters the Tiller Community.

Through the Tiller Money Labs add-on, users can share custom-built templates. This collaborative approach has yielded tools tailored to specific niches, such as the Financial Independence, Retire Early (FIRE) movement, real estate investors tracking rental income, and small business owners managing tax deductions.

Implications: The Future of Personal Finance and Open Banking

The growth of services like Tiller Money highlights a broader shift in how consumers interact with their financial data.

The Decline of Monolithic Software and "Walled Gardens"

The closure of legacy tools like Mint.com and the rising costs of traditional software like Quicken have exposed the vulnerabilities of closed personal finance ecosystems. When a proprietary platform changes its monetization strategy, updates its user interface, or shuts down entirely, users often lose years of historical data and customized workflows.

By leveraging open formats like Google Sheets (.gsheet) and Microsoft Excel (.xlsx), Tiller ensures that even if a user cancels their subscription, they retain complete, permanent ownership of their historical financial workbooks.

Proprietary Apps (e.g., Mint, Quicken)

[User Data] ---> [Proprietary Database] ---> [Closed UI]

*If the app shuts down, access to data is lost.*

Tiller Money Ecosystem

[User Data] ---> [Tiller Data Pipeline] ---> [Standard Excel/Google Sheet]

*If Tiller is canceled, the spreadsheet and historical data remain fully accessible.*The Rise of Open Banking Frameworks

Tiller’s reliance on secure APIs points to the future of global banking. As open banking regulations (such as PSD2 in Europe and similar market-driven initiatives in North America) gain traction, financial institutions are under increasing pressure to provide secure, standardized data access to consumers.

Tiller is well-positioned to benefit from this regulatory shift, which will likely result in faster data refreshes, fewer connection drops, and more robust authentication methods.

The Psychology of Financial Engagement

Behavioral economics suggests that passive financial tracking—where apps simply send automated push notifications about spending habits—rarely leads to lasting behavioral change.

By requiring users to engage directly with their spreadsheets, categorize outlier transactions, and build their own budget models, Tiller fosters a more active relationship with money. This hands-on approach helps users better understand their cash flow, optimize their debt payoff strategies, and make more informed long-term investment decisions.