Market Re-alignment: How Energy Relief and Hawkish Fed Policy Are Reshaping ETF Portfolios

The exchange-traded fund (ETF) landscape underwent a seismic shift this past week, as a combination of easing geopolitical tensions in the energy sector and a hawkish pivot from the Federal Reserve prompted a wholesale re-evaluation of investor risk exposure. As market participants recalibrated their portfolios to account for a "higher-for-longer" interest rate environment, capital flowed aggressively out of defensive, income-oriented vehicles and into broad-market, low-cost equity strategies.

The week served as a masterclass in macroeconomic sensitivity, demonstrating how quickly market sentiment can pivot when the dual levers of commodity pricing and monetary policy are pulled in opposing directions.

The Chronology of a Market Pivot

The week began under a shroud of optimism. Reports of a diplomatic breakthrough regarding the U.S.-Iran conflict signaled a potential de-escalation of tensions in the Middle East. With the promise of reopening critical global supply routes—most notably the Strait of Hormuz—oil prices experienced a sharp decline. For the equity markets, this was a signal to breathe.

Monday and Tuesday: The Energy-Driven Rally

As energy prices tumbled, the market reaction was instantaneous. Investors, long burdened by the inflationary pressures of high energy costs, pivoted toward small- and mid-cap equities. These sectors are historically the most sensitive to raw operating costs; lower energy prices directly translate to margin expansion for smaller firms. Consequently, capital flooded into funds like the Vanguard Mid-Cap ETF (VO), which saw a staggering $6.8 billion in inflows, and the Vanguard Small Cap ETF (VB), which attracted $4.2 billion.

Wednesday: The Warsh Effect

The tone shifted abruptly on Wednesday following the conclusion of the Federal Reserve’s first policy meeting under the chairmanship of Kevin Warsh. While the decision to hold interest rates steady was largely anticipated, the accompanying rhetoric proved to be a catalyst for renewed volatility. Chairman Warsh’s commentary indicated that despite the current stability, future rate hikes remain a viable tool in the Fed’s arsenal to combat stubborn inflation.

This hawkish stance acted as a "cold shower" for speculative growth plays, particularly in the tech sector, while simultaneously reinforcing the appeal of value-oriented, broad-market indices. The Fed’s assessment that the economy is "expanding at a solid pace" provided just enough comfort for investors to maintain exposure to core equities, albeit with a tactical shift toward higher-quality, value-based holdings.

Supporting Data: The Anatomy of Inflows and Outflows

The structural dominance of Vanguard’s low-cost equity ecosystem was the defining narrative of this week’s movement. In an environment defined by uncertainty, institutional and retail investors alike retreated to the safety of low-fee, broad-market index products.

The Rise of Broad-Market Vehicles

Vanguard’s dominance was total, capturing seven of the top 10 spots for weekly inflows. The scale of the movement into the Vanguard Mid-Cap ETF (VO) and the State Street SPDR Portfolio S&P 500 ETF (SPYM)—the latter of which pulled in $4.3 billion—suggests a massive rotation out of tactical positions and into core, set-it-and-forget-it holdings.

The Vanguard Value ETF (VTV) also benefited significantly, adding $3.8 billion. This movement underscores a specific investor sentiment: a desire for equity participation that is shielded from the volatility of pure-growth sectors while still capturing the upside of a solid domestic economy.

The Exodus from Defensive Income

Conversely, the "higher-for-longer" interest rate narrative proved catastrophic for traditional defensive income strategies. As the cost of borrowing remains elevated, the relative appeal of dividend-paying equities diminishes, especially when risk-free alternatives begin to offer more competitive yields.

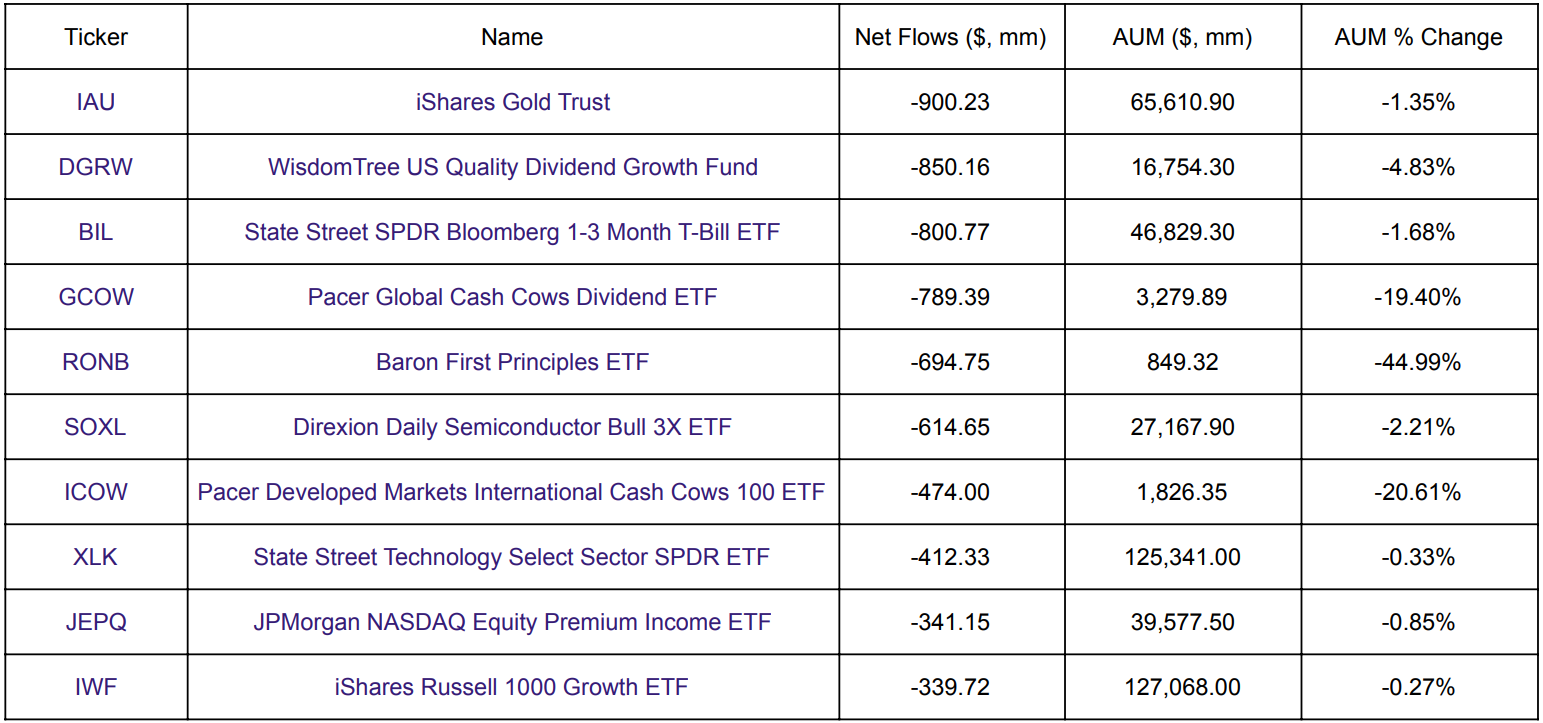

The iShares Gold Trust (IAU) saw $900.2 million in outflows, reflecting a decline in demand for non-yielding hedges. Similarly, cash-equivalent strategies such as the SPDR Bloomberg 1-3 Month T-Bill ETF (BIL) shed $800.8 million, as investors rotated funds away from "parking" capital and back into active market participation.

Perhaps most notable were the outflows from dividend-growth funds. The WisdomTree US Quality Dividend Growth Fund (DGRW) bled $850.2 million, signaling that investors are becoming increasingly discerning about the "quality" of their yield in a high-rate environment.

Editor’s Note: The Pacer Global Cash Cows Dividend ETF (GCOW) recorded a sharp outflow of $789.4 million, or 19.4% of its total assets. However, market analysis confirms this was primarily driven by a technical index rebalance, with capital flowing back into the fund in the subsequent trading session.

Official Stance and Market Implications

The Federal Open Market Committee (FOMC) maintains that the current economic expansion is robust enough to withstand further monetary tightening. For the average investor, this represents a transition from the "easy money" era of the previous decade to a regime of capital discipline.

The Tech Sector’s Correction

The most significant casualty of this hawkish pivot was the technology sector. Highly concentrated, premium-valuation tech plays found themselves on the chopping block as investors locked in profits. The Technology Select Sector SPDR ETF (XLK) saw $412.3 million in outflows, while the leveraged Direxion Daily Semiconductor Bull 3X ETF (SOXL) suffered a $614.7 million liquidation.

This behavior indicates that institutional investors are trimming their most aggressive positions to reduce volatility. When interest rates stay higher for longer, the discounted cash flows of high-growth tech firms are penalized, making them less attractive relative to the steady performance of value-oriented sectors.

The "Higher for Longer" Reality

The primary implication of the current market structure is a narrowing of the "alpha" gap. As the Fed signals that it is not yet ready to pivot toward rate cuts, the market is effectively being forced to price in a higher cost of capital.

For the ETF market, this suggests:

- Fee Sensitivity: Investors are increasingly gravitating toward low-cost, passive vehicles to maximize net returns in a lower-yield environment.

- Value Over Growth: As long as interest rate uncertainty persists, the rotation from speculative tech into value-oriented equities is likely to continue.

- Geopolitical Sensitivity: While the energy crunch eased this week, the sensitivity of the market to Middle Eastern supply lines remains a persistent "tail risk" that could cause rapid reversals in flows should the situation deteriorate.

Looking Ahead: Managing Risk in a Hawkish Cycle

As we look toward the remainder of the quarter, the primary challenge for the ETF industry will be managing the expectations of a cohort of investors who have become accustomed to frequent Fed pivots. Chairman Warsh’s debut has effectively reset the baseline expectation for monetary policy.

The movement into the Vanguard Mid-Cap (VO) and Small Cap (VB) funds suggests that investors are looking for domestic growth drivers that are not tied to the volatile tech sector. By focusing on the broader mid-market, investors are betting on the resiliency of the American consumer and the adaptability of domestic firms to navigate a high-rate environment.

However, the rapid outflows from defensive vehicles like IAU and DGRW serve as a warning. The "defensive" playbook of the last two years—gold and high-dividend yielders—is currently being rewritten. Investors are demanding a higher "risk premium" for their capital, and they are willing to rotate aggressively to find it.

Final Thoughts

This past week has underscored the fragility of the current market equilibrium. While the decline in oil prices provided a welcome cushion for operating margins, the looming reality of a hawkish Federal Reserve ensures that the path forward will not be without volatility. For the ETF industry, this means a period of high turnover, where the "winners" are those funds that can successfully balance the need for growth with the discipline of value-based, low-cost indexing.

As investors prepare for the next FOMC meeting, the mantra remains clear: follow the capital, monitor the energy corridors, and stay prepared for the inevitable re-calibration that accompanies a changing monetary guard.

For more news, information, and analysis on the evolving ETF landscape, visit VettaFi | ETF Trends.