Rethinking the Golden Years: A New Paradigm for Retirement Stability

For four decades, the financial services landscape has been defined by rigid silos. As an innovator who helped pioneer the "Accumulator"—a product that introduced downside protection to variable annuities and ultimately catalyzed a $1 trillion industry—I have spent my career observing how retirees interact with their money. Yet, as we approach 2028, the traditional pillars of retirement planning are under unprecedented pressure.

With longevity increasing and inflation eroding purchasing power, the modern retiree faces a "perfect storm" of challenges: volatile Social Security outlooks, rising medical costs, and an impending shift in federal policy that threatens the stability of middle-class home ownership. To survive this environment, we must move beyond the antiquated "4% to 5% withdrawal" rule and embrace a more integrated, holistic approach to wealth management.

The Impending Medicaid Crisis: A New Hurdle for Homeowners

The most pressing concern on the horizon is a subtle but seismic shift in federal Medicaid policy. Beginning in 2028, a new regulation will cap allowable home equity at $1 million for Medicaid long-term care (LTC) eligibility.

Currently, state-level rules provide a buffer, with allowable equity thresholds ranging from $750,000 to $1.13 million, often adjusted annually for inflation. By centralizing this cap at $1 million and stripping away the inflation index, the government is effectively tightening the net around the "mass affluent"—those who have worked a lifetime to pay off their homes in high-cost-of-living areas. For these individuals, the prospect of needing nursing home care is no longer just a health concern; it is a potential threat to their primary asset.

Chronology of a Shifting Landscape

- The 1980s–2000s: The rise of the variable annuity and the "Accumulator" era, which focused on market participation with downside protection.

- 2010s: Increased focus on the "4% rule" as the gold standard for retirement income sustainability.

- 2024: Mounting evidence, such as the Schroders study on the affordability crisis, highlights that inflation and medical costs have rendered standard withdrawal models obsolete for many.

- 2028: The implementation of the federal $1 million home equity cap for Medicaid eligibility, significantly limiting the planning flexibility of middle-class retirees.

The Data: Why Current Models Fail the Retiree

The math behind the current retirement crisis is stark. According to data from the Administration for Community Living, 50% of retirees aged 85 and older will require some form of long-term care. With costs currently ranging between $80,000 and $150,000 per year—and rising at an annual rate of 3% to 5%—the math does not favor the traditional "investment-only" portfolio.

For an average retiree with a $2 million net worth split between a rollover IRA and their home, long-term care costs can consume 25% of their total wealth in just a few years. Without a proactive strategy to unlock home equity, many retirees will be forced into a "fire sale" of their homes, incurring unnecessary capital gains taxes and losing the very asset that provides them shelter and security.

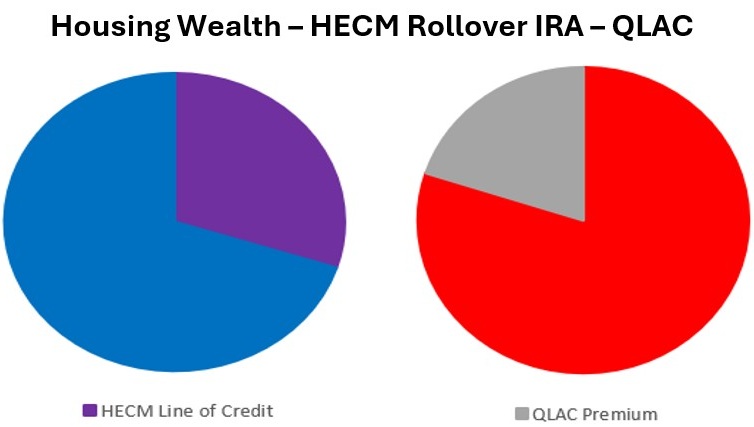

Introducing "HomeEquity2Income" (H2I)

To address these systemic vulnerabilities, I have developed a strategy that breaks down the silos between investments, annuities, and housing wealth. We call this framework HomeEquity2Income (H2I).

The strategy relies on two underutilized vehicles:

- Home Equity Conversion Mortgages (HECM): A specialized reverse mortgage that allows homeowners to tap into their home’s value without the immediate burden of repayment.

- Qualified Longevity Annuity Contracts (QLAC): A powerful tool that allows retirees to defer taxes on a portion of their IRA and guarantees a stream of income starting at a later age.

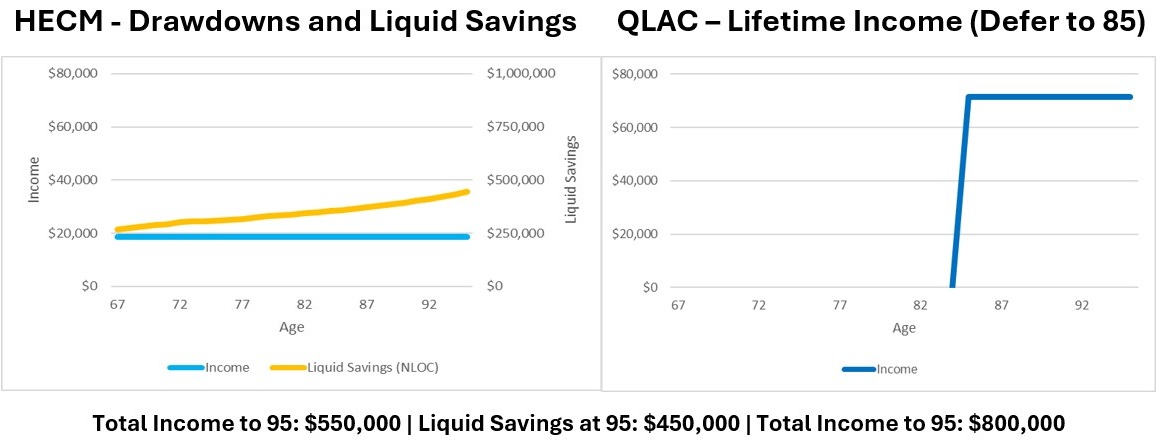

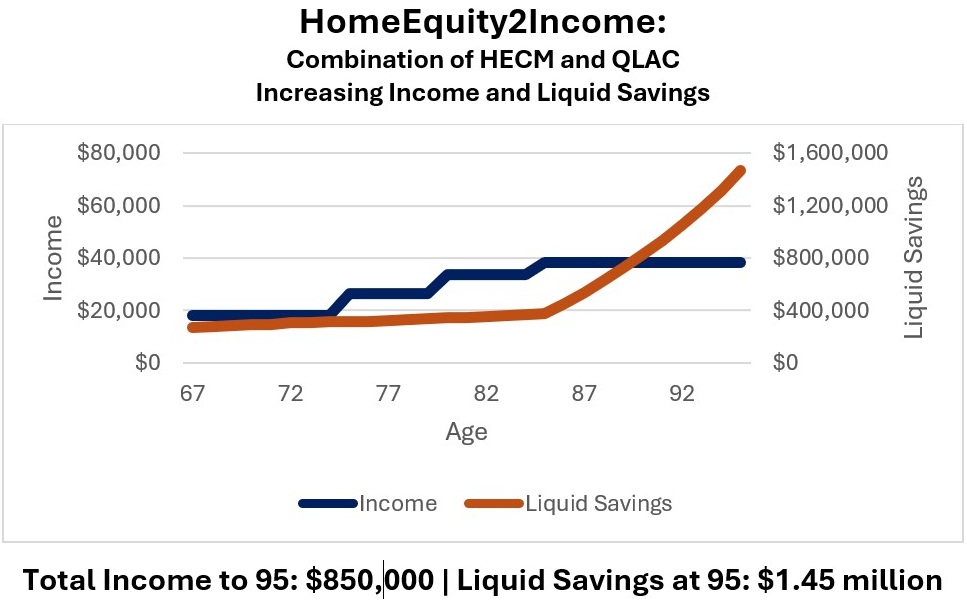

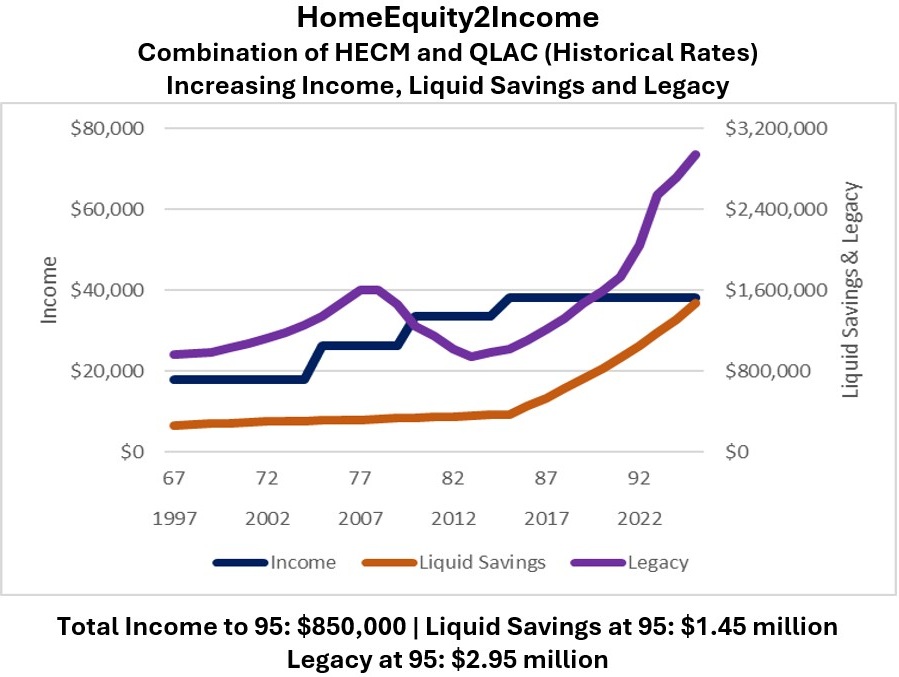

The Synergistic Effect

Individually, these products are often misunderstood. The HECM is frequently criticized for its high costs and the risk of over-borrowing, while the QLAC is often dismissed due to its lack of liquidity. However, when integrated into a single algorithm, they solve each other’s weaknesses. The HECM provides the liquidity required to cover immediate costs, while the QLAC secures long-term income, allowing the retiree to avoid prematurely depleting their liquid IRA savings.

Official Perspectives and Regulatory Context

From a regulatory standpoint, the beauty of the H2I model is that it requires no legislative intervention or new financial products. It is an architectural change in how we view the "balance sheet" of a retiree.

While financial advisors have traditionally treated home equity as an untouchable asset, the current economic climate demands a shift toward treating it as a core component of the income portfolio. Financial institutions are increasingly seeing the benefit of these combined strategies, though the onus remains on the advisor to implement them with a high degree of mathematical precision. By leveraging the existing tax-deferred status of QLACs and the structural flexibility of HECMs, we are essentially building a defensive wall around the retiree’s liquid assets.

Implications for Long-Term Care and Legacy

The implications of H2I for the average retiree are twofold:

- Medicaid Protection: By properly structuring the HECM and QLAC, retirees can manage their income and assets in a way that avoids the need to "spend down" to qualify for Medicaid, effectively preserving more of their legacy for their heirs.

- Aging in Place: Perhaps most importantly, this model supports the ability of seniors to remain in their homes. Instead of selling the house to pay for care, the home becomes a financial engine that generates the necessary cash flow to support home-based care or assisted living services.

Scenario Testing: A Case Study

In a hypothetical plan for a retiree with $800,000 in a rollover IRA, $1 million in personal savings, and a home worth $1 million, we can project a starting income of $133,000 (plus $36,000 in Social Security). When we integrate H2I, the model accounts for inflation-adjusted growth and potential long-term care scenarios.

The results consistently show that retirees can maintain a higher standard of living while simultaneously creating a reserve for late-life care. This isn’t about gaming the system; it’s about utilizing the tools currently available to solve the reality of modern longevity.

A Call for Strategic Planning

For too long, the retirement industry has sold products in isolation. We have sold the annuity as a separate piece of the puzzle, and we have treated the home as a separate asset class. This "silo" mentality is a disservice to the millions of Americans who are currently navigating the transition into their retirement years.

The H2I framework demonstrates that the solution to our current retirement crisis isn’t found in a new product, but in a new design. It is about taking the building blocks we already have—home equity, retirement savings, and longevity protection—and assembling them into a cohesive structure.

As we look toward 2028 and the changing landscape of Medicaid, the message is clear: the time for passive, traditional retirement planning has passed. It is time for retirees to become architects of their own security. By taking a comprehensive look at their entire net worth, including the home, and utilizing the power of longevity-focused annuities, retirees can achieve the dual goals of increased income and greater financial independence.

For those ready to move beyond the status quo, the tools for a more robust, stable retirement are already in your hands—they simply need to be organized.