The Digital Shift: Why Online Retail Is Outpacing Traditional Commerce Despite Economic Headwinds

In an economic climate defined by persistent inflation and a "higher-for-longer" interest rate environment, conventional wisdom might suggest that consumer spending would retreat. Yet, the data tells a different story. While brick-and-mortar storefronts grapple with the crushing weight of rising operational costs and shifting foot-traffic patterns, consumers are decisively migrating to digital channels. This structural evolution in how the world shops is creating a massive tailwind for e-commerce, offering a unique landscape for investors looking to navigate the retail sector beyond traditional market-cap-weighted giants.

The Resilience of the Consumer: A Macro Overview

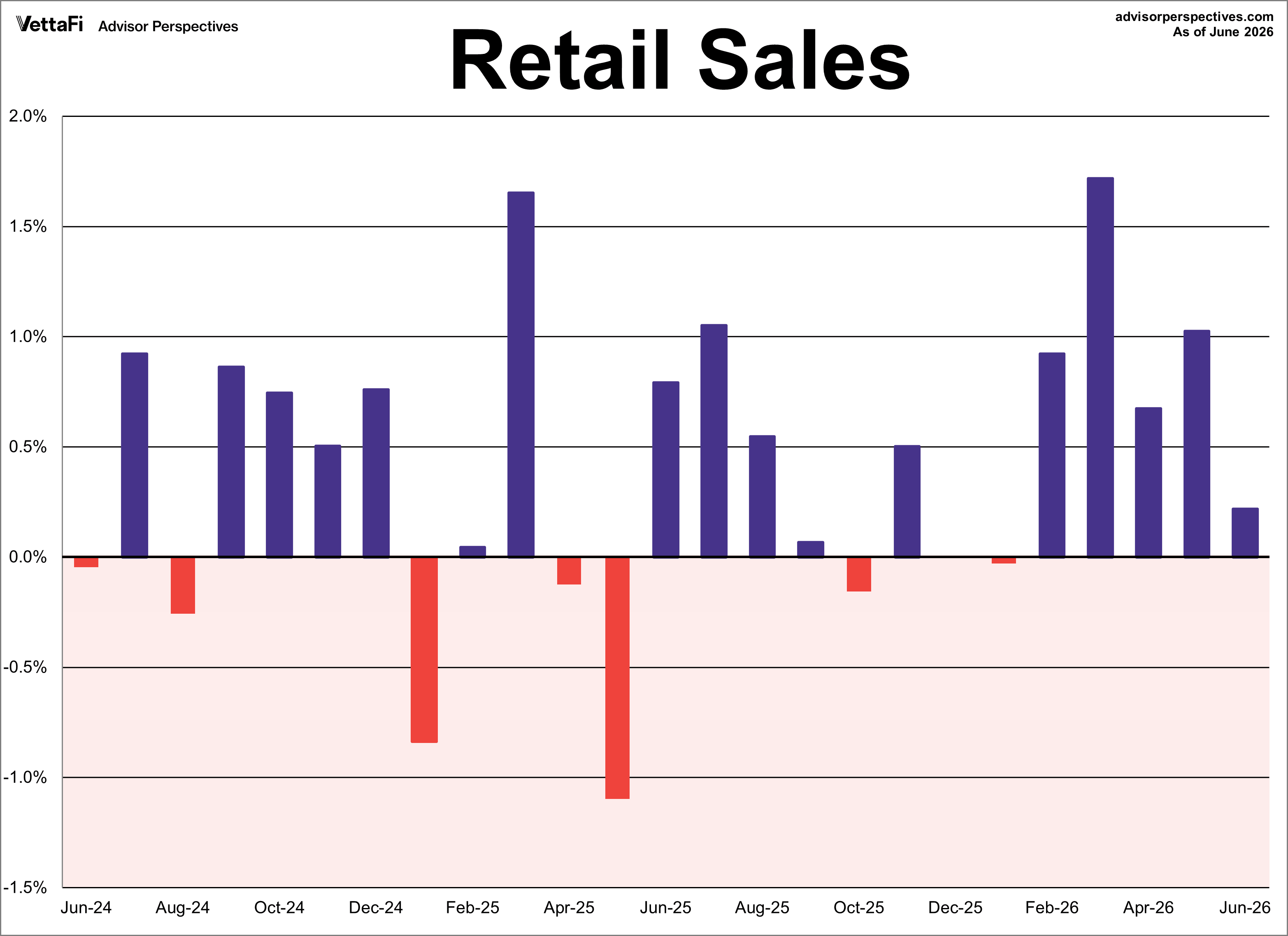

The latest analysis from TMX VettaFi economic research analyst Jen Nash highlights a paradox: while macro headwinds remain, retail sales have demonstrated remarkable resilience. According to the U.S. Census Bureau’s Advance Retail Sales Report, consumer spending has notched five consecutive monthly gains, with headline sales ticking up 0.2% in June alone.

This spending, however, is not uniform. The friction of high interest rates has acted as a filter, pushing price-conscious and convenience-seeking consumers toward the digital ecosystem. The growth in e-commerce is not merely a post-pandemic artifact; it is a fundamental shift in the global supply chain and the consumer experience.

Chronology of the E-Commerce Surge: From 2020 to 2030

The trajectory of online retail has been one of exponential acceleration. To understand the current market, one must look at the timeline of its expansion:

- 2020–2022 (The Acceleration Phase): The global pandemic served as a catalyst, pulling years of digital adoption forward into a few months. During this period, e-commerce became the primary, and often sole, lifeline for retail commerce.

- 2023–2024 (The Normalization and Integration Phase): As physical stores reopened, the market didn’t retract to pre-pandemic levels. Instead, it moved toward an omnichannel model. The "digital-first" consumer became the standard, with mobile shopping and social commerce becoming the dominant drivers.

- 2025 (The Trillion-Dollar Milestone): Global online shopping revenue reached a staggering $6.42 trillion. This year solidified the digital storefront as the primary engine of the global economy.

- 2026 and Beyond (The Expansion Phase): Current data from Q1 2026 shows that seasonally adjusted U.S. e-commerce sales reached a record $326.7 billion. This represents a 9.8% year-over-year surge, significantly outpacing the 3.9% growth rate of total retail sales.

- 2030 Projection: Industry forecasts indicate that global online retail revenue is on track to surpass $8.9 trillion, with an average annual growth rate of approximately 6.79%.

Supporting Data: The Quantitative Case for Digital Retail

The quantitative evidence supporting the dominance of e-commerce is overwhelming. When comparing total retail sales growth to e-commerce-specific growth, the gap is widening. In the first quarter of 2026, while the broader retail sector showed signs of maturation at 3.9%, e-commerce outperformed it by nearly 600 basis points.

This is further corroborated by midyear performance markers. Amazon’s Prime Day event in late June 2026 serves as a definitive case study in modern consumer behavior. In a four-day window, U.S. online spending skyrocketed to $26.4 billion—a 9.3% increase compared to the previous year.

Perhaps more significant than the headline numbers is the "copycat effect" observed among competitors. Retail giants like Walmart and Target have responded by launching aggressive, promotional digital events during the same window. This creates a "rising tide" scenario where the entire digital ecosystem benefits from increased consumer traffic, particularly in discretionary categories such as high-end electronics, home goods, and toys. As consumers hunt for value, they are increasingly willing to spend on higher-ticket items, provided they can secure them through digital portals that offer price transparency and ease of comparison.

The Investment Dilemma: Concentration Risk vs. Diversification

For investors seeking to capture this tailwind through retail-focused ETFs, a significant structural trap exists. Most traditional retail ETFs are market-cap-weighted. By their very design, these funds allocate the vast majority of their assets to a handful of "mega-cap" companies. While these giants are instrumental to the sector, this concentration exposes investors to idiosyncratic risk—if a single giant falters, the entire portfolio’s performance is compromised.

This has led to a growing interest in more balanced, high-conviction strategies. The Amplify Online Retail ETF (IBUY) provides a compelling alternative. Rather than blindly following the market-cap leaderboard, IBUY employs a methodology that seeks to capture the growth of the entire digital retail value chain.

Understanding the IBUY Methodology

IBUY utilizes the EQM Online Retail Index, which screens for publicly traded companies deriving a significant portion of their revenue from online transactions. The index structure is segmented into four critical pillars:

- Traditional Online Retail: The classic e-commerce storefronts.

- Online Travel: A massive, high-margin sector that is increasingly digital-first.

- Online Marketplaces: Platforms that connect buyers and sellers globally.

- Omnichannel Retail: Traditional retailers that have successfully pivoted to a hybrid digital-physical model.

By using a modified equal-weighting methodology, IBUY ensures that a company’s influence on the portfolio is not determined solely by its size, but by its relevance to the digital retail theme. This allows for meaningful exposure to mid- and small-cap innovators—the companies often responsible for the next wave of technological disruption—alongside established household names like Amazon, Wayfair, Etsy, and Hims & Hers Health.

Implications for the Future of Retail

The implications of this shift are profound for both the investor and the consumer. For the investor, the "retail" sector is no longer synonymous with the local mall; it is now a technological sector characterized by data analytics, logistics, and global supply chain management.

For the consumer, the trend is toward frictionless, 24/7 access to global markets. As digital platforms continue to integrate social media, augmented reality (AR) for virtual fittings, and AI-driven personalized recommendations, the barrier between "browsing" and "buying" will continue to dissolve.

The Macro View: A Global Economic Storefront

The projection that global online transactions will climb at an average annual rate of 6.79% through 2030 suggests that we are still in the early innings of this transition. Emerging markets, which are currently undergoing rapid digitalization, will likely become the next frontier for these platforms. Investors who diversify across the global online retail landscape are not just betting on a specific stock; they are betting on the fundamental infrastructure of 21st-century commerce.

Conclusion

The evidence presented by the Census Bureau and industry researchers is clear: the digital transformation of retail is not a temporary trend but a permanent structural realignment. While the broader economy may continue to grapple with inflationary pressures, the efficiency and accessibility of online marketplaces provide a compelling value proposition that consumers are unwilling to abandon.

For the modern investor, the challenge is to move past the allure of top-heavy market-cap indices and embrace a more nuanced, diversified approach. By focusing on the broader ecosystem of digital retail—from the platforms that facilitate the transactions to the companies that drive the consumer experience—investors can better align their portfolios with the future of global consumption. As we look toward 2030, the "digital storefront" is not just an alternative to physical retail; it is, quite simply, the economy.

Disclaimer: For more news, information, and analysis, visit the Thematic Investing Content Hub. VettaFi LLC (“VettaFi”) is the index provider for IBUY, for which it receives an index licensing fee. However, IBUY is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of IBUY. This article is for informational purposes only and does not constitute financial advice.